The Ultimate Guide to the Best Jewelry Insurance Companies

Our jewelry insurance guide reviews the policies of the top eight companies. Learn what to look for so you can find the coverage that’s right for you.

17 Minute Read

But have you thought about jewelry insurance?

In most cases, insuring your jewelry is absolutely worth it. For most of us, jewelry is a significant purchase, sometimes the largest (or second largest) purchase in our lives. Let me ask you, how much did you spend on that engagement ring, earrings, or watch? Would you be able to replace the item completely out of pocket? Generally, the answer is "Yes, I would be able to replace the jewelry" — but it would be extremely expensive and painful.

What if we told you that you can insure that piece of jewelry for only a small percentage of the value? Well, you can. Specialized companies, like BriteCo Jewelry Insurance, for example, can offer you impressive diamond ring insurance coverage for as low as 0.5%-1.5% of your item's total value, annually.

The Top 8 Jewelry Insurance Companies

To make your life easier, we've put together the ultimate guide to the best jewelry insurance companies. Think of it as your one-stop shop for all things jewelry insurance related. We've researched the entire market and selected the eight best jewelry insurance companies to keep you covered in the event of jewelry loss or damage.

Specialized Jewelry Insurance

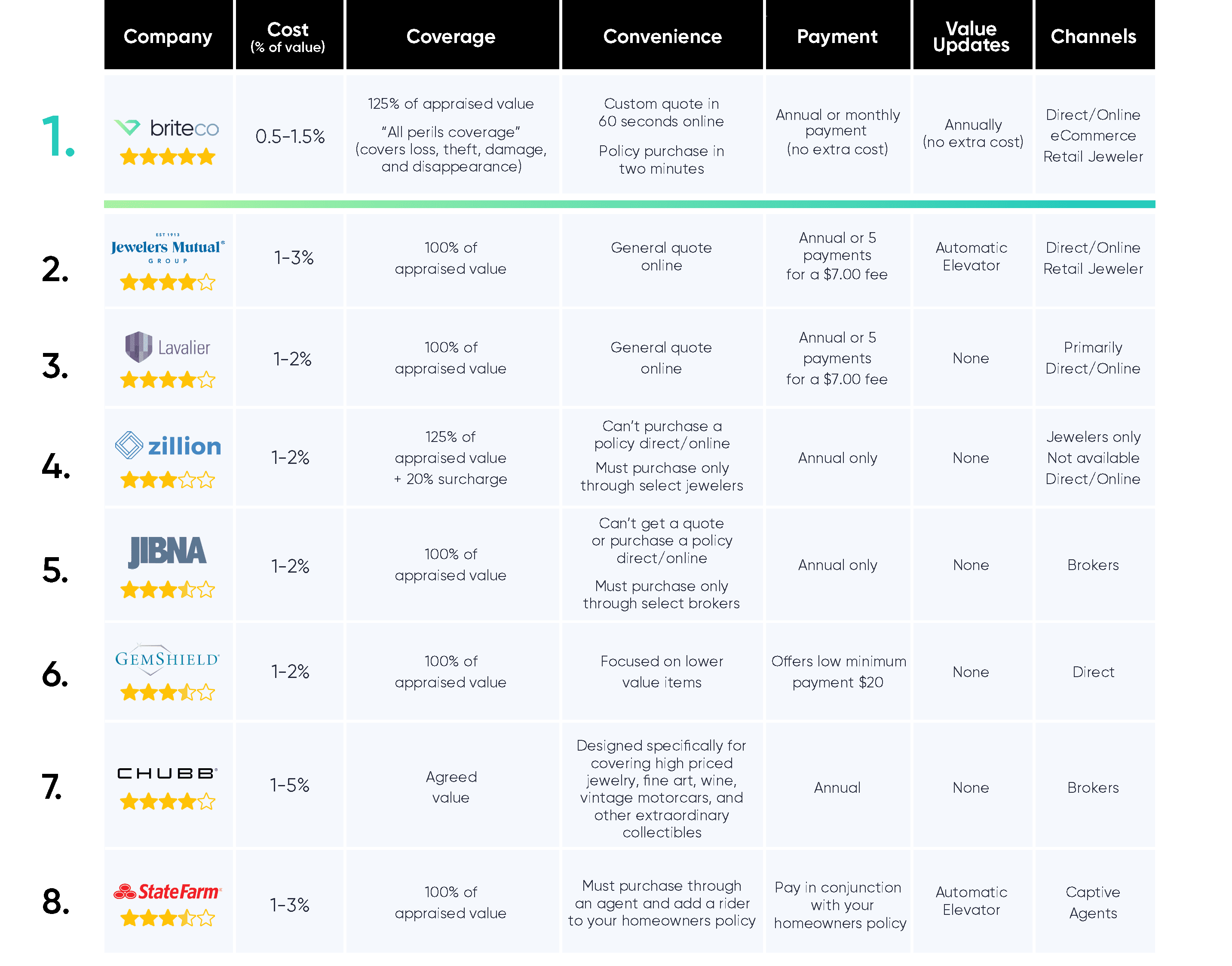

#1 BriteCo Jewelry Insurance — Best Overall Value

#2 Jewelers Mutual Insurance Company — Oldest, Well-Established Jewelry Insurer

#3 Lavalier — Best for Less Expensive Jewelry

#4 Zillion — Best Value Indirect Insurer

#5 JIBNA — Best for Antique or Highly Customized Jewelry

#6 GemShield — Best Basic Jewelry Coverage

Non-Specialized Insurance

#7 Chubb — Best High-End Insurance

#8 State Farm Insurance — Best for Bundling Jewelry Under $5,000

Types of Jewelry Insurance

Before diving into each company, it's important to understand your options and how jewelry insurance works. The two main types of jewelry insurance policies are:

- A specialized or stand-alone jewelry insurance policy.

- A scheduled item on your homeowners insurance policy. This is sometimes referred to as an endorsement, a rider, or a floater.

Specialized Jewelry Insurance

A specialized jewelry insurance policy is specifically designed for insuring jewelry. If you're looking for the absolute best jewelry insurance coverage, a specialized policy is the right choice. Because it's a very specific coverage tailor-made to a piece of jewelry or a watch, you'll get additional coverage you may not get with a homeowners rider. Additionally, it's most often the smarter money-saving option.

Generally, we recommend not tying your jewelry to your homeowners policy.

Mysterious Disappearance Coverage

Many homeowners riders don't cover "mysterious disappearance." You'll definitely want this important coverage, since most losses fall under this category. Imagine your ring simply disappeared from your gym bag. Was it stolen or did you lose it? You're not really sure. You don't even know exactly when it happened. You'll want coverage for this. The better specialized jewelry insurance policies will cover this.

Claims Can Affect Your Insurance Credit Score

Before choosing a policy, you should consider coverage value limits and coverage for damage (not only a pure loss). You should also learn how your claims will impact your insurance credit score.

You have an insurance credit score, distinct from other personal credit scores, like your FICO score. It's very important — and no one talks about it. When you file a claim, some insurance companies will actually report your loss to a reporting agency. As a result, your rates will increase. A reported loss can stay on your insurance credit report for 5-7 years.

Just like any credit score, you need to keep this score as high as possible. If you have a jewelry loss, most homeowners insurance companies will report this loss, so your homeowners rates will increase. In the worst-case scenario, your homeowners could actually drop you. Some specialized insurance companies will also report claims.

Homeowners Insurance Coverage

Most homeowners policies do have some sort of inherent coverage for jewelry, as it does for some other household items. However, problems may arise because a homeowners policy wasn't really meant to include jewelry, watch, and ring coverage. This usually results in coverage gaps and incomplete coverage. If you're purchasing jewelry insurance, make sure you're fully covered. We detailed a few issues above, like "mysterious disappearance," but there are more things to take into consideration.

Deductibles

Let's talk about deductibles. Insurance companies introduce deductibles to reduce your monthly or annual premium payment. In turn, when a loss or damage occurs, you have to cover a specific portion of the claim out of pocket. This could be a sizable amount, especially if it's a percentage of the claim. Since the difference in premium payment is typically minimal, we usually recommend opting for a zero-deductible plan.

When is Umbrella Coverage Preferable to Specialized Insurance?

We don't recommend specialized jewelry policies in all cases. For instance, we wouldn't recommend purchasing a specialized jewelry policy if you had a schedule of $500,000 and had other assets such as boats, art, etc. We would recommend an umbrella carrier. However, for most cases, we recommend a specialized jewelry insurance policy.

Specialized Jewelry Insurance Comparison

If you're ready to shop for specialized jewelry insurance coverage, you're in luck. We've researched the best jewelry insurance companies, so you can make an informed decision based on your situation.

When comparing the best jewelry insurance companies, we took multiple factors into account, such as their AM Best credit and company rating, how long they've been in business, coverage offered, known limitations, and any other competitive advantages one company may have over the others.

#1 BriteCo Jewelry Insurance — Best Overall Value

Established in 2017 by a third-generation jeweler, BriteCo is our top choice for best overall value. BriteCo has quickly become renowned in the industry as the first insurtech company that specializes solely in insuring fine jewelry and watches.

Because they're an online-only insurer, BriteCo has no local offices or hundreds of affiliated agents, like a traditional carrier. While this may seem odd, BriteCo's innovative approach makes shopping for jewelry insurance easy.

Obtaining a quote is as simple as clicking a link and entering some information about the type of jewelry you wish to insure as well as your location. With your smartphone, it takes less than a minute to get a free, instant quote for AM Best A+ rated coverage and less than 5 minutes to purchase a policy. Their online interface is top-notch, and there's no app to download. You can easily access policy services through the company's website (including filing a claim).

Trusted by thousands of jewelers across the USA, BriteCo has the best overall coverage of the companies we surveyed. Surprisingly, they're also one of the most affordable. For example, BriteCo's average policy rates typically undercut their competitors' rates, and they also offer monthly premium payment options starting at less than $5 per month. In fact, BriteCo has revolutionized the way fine jewelry and watches are insured, with rates at only 0.5-1.5% of a piece's value compared to the industry standard of 1-3%.

Insuring with BriteCo feels more like a Netflix subscription than a stuffy insurance policy. Nevertheless, their replacement-only policies are the best available, since they have zero deductible and cover your jewelry up to 125% of its appraised value at no additional cost.

BriteCo Jewelry Insurance — Key Highlights

- Top choice of the International Gem Society, with insurance rates below competitors' for better coverage.

- AM Best A+ rated jewelry insurance policies underwritten by GIC.

- Worldwide coverage for U.S. residents against major perils: loss, damage, theft, and mysterious disappearances.

- Zero-deductible, replacement-only policies with lowest rates on average, which means the best specialized jewelry insurance coverage available is also among the most affordable.

- Annual coverage periods payable up-front with a 5% discount, or convenient, low monthly premium payments starting below $5/month.

- Automatically covers up to 125% of the appraised value (that's an additional 25% of coverage at no extra cost).

- Covers your significant other without the need for additional verification. (Won't ruin a surprise proposal).

- Coverage for preventative maintenance included without a deductible.

- Only specialized online jewelry insurer with flexible, small monthly payments.

- Ample limits, with coverage up to $150,000 per item/$350,000 total schedule value per individual.

- Easy, straightforward claims process allows you to work with your local jeweler.

- Automatically keeps appraised values up to date on a yearly basis.

- Jewelers of America (JA) partner, and trusted by over 2,000 independent retail jewelers across the USA.

- Licensed in all 50 states plus the District of Columbia.

#2 Jewelers Mutual Insurance Company — Oldest, Well-Established Jewelry Insurer

Jewelers Mutual was founded in 1913 by a group of Wisconsin jewelers who wanted to solve jewelry store owners' insurance needs. For more than 100 years, Jewelers Mutual has billed itself as the only company that insures the jewelry industry, with Jeweler's Block coverage (insurance for jewelry stores) being the largest portion of their overall portfolio. Nowadays, they offer among the best direct coverage for individual policyholders, especially for those with unique, highly customized pieces, like custom Rolexes.

Like BriteCo, Jewelers Mutual offers replacement-only insurance policies, but the policies don't provide coverage above 100% of the appraised value of your jewelry. However, they do cover the same major perils.

Jewelers Mutual earns a top spot on our list because their customers can choose whether to have a deductible. While some customers insist on coverage with no out-of-pocket expenses, others favor setting a deductible to lower their annual premiums, especially when insuring higher-risk items. (Again, we usually recommend opting for zero-deductible policies).

Jewelers Mutual Insurance Company — Highlights

- Well-established, over 100-year-old company.

- AM Best A+ rated.

- Perfect for one-of-a-kind pieces, including high-dollar custom pieces and luxury watches with aftermarket stones.

- Offers worldwide protection against: loss, damage, theft, and mysterious disappearances.

- Offers different deductible limits to offset insurance rate costs.

- Replacement-only policies repair or replace insured items with those of like kind and quality, up to 100% of the appraised value.

- Will cover loose gemstones.

- Claims process that allows you to use your local jeweler.

- Annual pay with periodic payments available (for an extra fee).

#3 Lavalier — Best for Less Expensive Jewelry

A relative newcomer to jewelry insurance, Lavalier offers their customers the option to purchase "non-scheduled" coverage. Basically, this means you can insure less valuable pieces of jewelry. This is fantastic for people with heirloom or vintage jewelry with more sentimental than actual value, especially if they're in disrepair. With Lavalier, you can purchase non-scheduled coverage with an agreed value of less than $1,000, without an appraisal. For more traditional jewelry items or vintage pieces in excellent condition, Lavalier offers scheduled jewelry insurance policies limited to $50,000 per item.

We also like Lavalier's online interface. Obtaining a quote is a straightforward process that requires just a few pieces of information, like your ZIP code and the appraised value of your jewelry.

If you want to insure your watch, however, you should consider another insurer. Lavalier doesn't advertise men's or ladies' watch insurance but may offer it on a case-by-case basis.

Lavalier — Highlights

- AM Best A+ rated policies underwritten by Berkley Asset Protection.

- Offers scheduled/non-scheduled coverage for most fine jewelry except for men's or ladies' watches (case-by-case).

- Scheduled limited to $50,000 per item/unscheduled limited to $1,000 per item.

- Unscheduled items less than $1,000 don't require an appraisal.

- Exclusions apply, but Lavalier's all-risk coverage includes major perils: loss, theft, damage, and disappearance.

- Deductible choices to offset annual insurance premiums.

- Claims process handled directly through your jeweler or by direct reimbursement (case-by-case).

- Annual or installment payments.

#4 Zillion — Best Value Indirect Insurer

Another relatively young insurance company, Zillion offers jewelry and watch insurance comparable to others on this list at competitive prices. While most insurers sell insurance directly — meaning you, the consumer, can shop for a quote on the open market — Zillion is now an indirect insurer. This means they control who receives an insurance quote, how it's received, and when.

Zillion has partnered with select jewelers across the United States to offer competitive insurance rates specifically to customers of their partner stores. Their online quote widget includes a disclaimer that reads, "Zillion partners with jewelers to offer their customers lower rates on [jewelry] insurance. If you don't see your jeweler on our list, we're sorry, we won't be able to offer you a quote for insurance."

In terms of coverage, Zillion's jewelry insurance policies are backed by AXA XL and cover all major perils.

Zillion — Highlights

- Indirect quotes only (must purchase through an approved jeweler).

- Underwritten by AXA XL, rated AM Best A+ Superior.

- Zero-deductible, worldwide coverage against major perils: loss, damage, theft, and mysterious disappearances.

- Appraisal not required for initial purchase but required upon a claim.

- Claims process requires you to go through your original jeweler.

- 30-day grace period for cancellation for full refund; prorated thereafter.

- No monthly pay option; annual pay only.

#5 JIBNA — Best for Antique or Highly Customized Jewelry

JIBNA stands for Jewelry Insurance Brokerage of North America. If you value relationships over convenience, and don't mind shopping for jewelry insurance like it's 1989, then you'll love JIBNA.

Unlike other specialized insurance companies on our list, JIBNA doesn't provide online quotes to shoppers. Instead, you'll need to find an authorized JIBNA insurance broker just to get a quote. While this presents a challenge for some, others might find it helpful. Since you must contact JIBNA insurance experts, they can guide you toward the best options for your situation. This is helpful, since JIBNA's coverage isn't one-size-fits-all.

In terms of coverage, JIBNA offers the best agreed-value coverage on this list. With an agreed-value policy, you aren't required to replace an insured item as the result of a qualified loss. Instead, the insurance company will write you a check for the agreed-upon insured value of the item, as determined by an appraisal or sales receipt. However, you'll also pay mightily for agreed-value policies. They can cost up to 50% more than replacement policies.

While not for everyone, this type of coverage may benefit people looking to insure ultra-rare, one-of-a-kind pieces or discontinued luxury watches, since the items being insured are virtually impossible to replace. Claim settlements are generally paid within a 60-day period.

The all-risk policy covers all major perils. Customers can also choose a deductible limit that's right for their situation. For new purchases, JIBNA gives temporary coverage of up to $10,000 per-item before a broker adds them to your schedule. Notably, JIBNA has some of the highest coverage limits available, up to $500,000 per item and $2,500,000 per individual schedule.

JIBNA — Highlights

- No online quotes; must contact a JIBNA-authorized broker.

- Agreed-value policies can cost much more than a normal replacement policy.

- Policies underwritten by an AM Best A rated carrier.

- All-risk agreed-value policies that cover major perils: loss, damage, theft, and mysterious disappearances.

- $1,000 actual cash value policy minimum for insured jewelry and watches.

- Great for antique or custom jewelry and other one-of-a-kind pieces that can't be replaced easily.

- Appraisals and sales receipts required to establish agreed value.

- High limits available up to $500,000 per item/$2.5M per schedule.

- Deductible options available.

- Doesn't cover loose gemstones.

- Annual pay only.

#6 GemShield — Best Basic Jewelry Coverage

Anyone in the jewelry industry will recognize the name GemShield. For decades, independent jewelry store owners have recommended GemShield to their customers for their personal jewelry insurance needs.

While far from the most comprehensive specialized jewelry insurance option, GemShield offers relatively low rates for basic jewelry insurance coverage against major perils. You'll save money, especially if you're insuring a piece valued under $2,000,

GemShield is underwritten by Wexler Insurance Agency, a wholly owned subsidiary of Jewelers Mutual Insurance Company.

GemShield — Highlights

- Offers online quotes or option to contact an agent.

- Policies underwritten by an AM Best A+ rated carrier.

- All-risk, agreed-value policies that cover major perils: loss, damage, theft, and mysterious disappearances.

- Coverage limited to only $35,000 per item/$100,000 per schedule.

- Items valued over $5,000 must have an appraisal no more than 18 months old; items less than $5,000 can be insured with a detailed sales receipt.

- Lowest minimum annual premium, only $20.

Non-Specialized Insurer Comparison

We strongly recommend insuring your fine jewelry and watches with a specialized jewelry insurance company. Of course, under some circumstances, it just makes sense to insure your valuables with a broader property and casualty company, such as your current homeowners or renters insurance carrier.

If you have a diverse and valuable asset portfolio or, conversely, own jewelry worth less than around $1,000, insuring your jewelry along with other possessions on your homeowners or renters insurance is likely your best option. You'll want something called a rider or floater, which functions like a separate schedule just for your jewelry and other valuables.

Here are some of the umbrella carriers we recommend.

#7 Chubb — Best High-End Insurance

If you're a high-net-worth-individual who requires some of the most comprehensive coverage money can buy (with premiums to match), then you may have heard of Chubb. Founded in 1792 and domiciled in Zurich, Switzerland, Chubb is the largest publicly traded property and casualty insurance company on the planet.

Chubb understands the unique needs of its clientele and offers a robust valuable articles rider called Chubb Masterpiece. Designed specifically for covering high-end jewelry, fine art, wine, vintage motorcars, and other extraordinary collectibles, Chubb Masterpiece brings peace of mind to customers, with worldwide coverage and zero deductible in most cases. In addition, newly acquired items are automatically covered, albeit at 25% of the itemized coverage for up to 90 days.

While we couldn't find exact term limits, individuals with personal articles valued at over $25,000 would be eligible for coverage under Chubb Masterpiece. Customers can also choose blanket coverage or an itemized schedule. For jewelry coverage, Chubb requires appraisals for individual jewelry pieces valued at $100,000 or more. For anything less, you'll only need to provide a detailed description of the piece you wish to insure along with its estimated value.

If you're unsure of what your jewelry might be worth, your Chubb agent will help you determine that. An agreed-value feature allows you to receive 100% of the insured value upon any covered jewelry loss. Under certain circumstances, customers may be eligible to receive up to 150% of the insured amount, itemized on the policy to compensate for increases in market value when applicable.

Chubb — Highlights

- Well-established, high-end property and casualty insurance company that offers a multitude of insurance lines, not specialized toward any specific category.

- Perfect for HNWIs looking for the best umbrella coverage.

- Established in 1792.

- Coverage Rated A+ Superior by AM Best.

- Largest publicly traded property and casualty insurance company.

- Agreed-value only policies offer worldwide coverage.

- Will receive up to 100% of your scheduled insured policy amount for lost or ruined jewelry.

- Claim payout up to 150% of your entire policy amount, possible in specific scenarios where insured item value has increased dramatically.

- Sub-limit of $5,000 for lost, stolen, or missing jewelry.

- Appraisals only required for jewelry items exceeding $100,000 in value.

- Policy not specific to jewelry; open to other high-value personal articles and collectibles as well, such as wine, spirits, and fine art.

- Must go through an agent, making it difficult to shop.

- Costly premiums, but worth it under the right circumstances.

#8 State Farm Insurance — Best for Bundling Jewelry Under $5,000

State Farm is a well-known, international insurance company with thousands of agents across the USA. As a major property and casualty insurance company, State Farm focuses primarily on auto and homeowner insurance policies. For insuring jewelry, State Farm uses what is known as a jewelry floater or a personal articles (PA) rider. This optional addition to its homeowners insurance policy protects against financial loss from damage or theft of itemized jewelry pieces.

Keep in mind that high deductibles for PA riders will make them more affordable but require out-of-pocket expense for claims. Also, since the riders are tied to your homeowners policy, any jewelry claims can affect coverage for your other property.

State Farm Insurance — Highlights

- Technically a personal articles policy; won't result in a multi-line discount from the carrier.

- Convenience of single-carrier coverage with a nationwide network of 18,000 agents.

- May offer a cash-out option versus replacement in the event of a claim.

Bottom Line: Don't Wait to Get Fine Jewelry, Watch, and Ring Insurance

By some estimates, more than half the engagement rings sold in the USA don't have ring insurance. In far too many cases, people assume their homeowners or renters insurance will cover any loss. However, after a loss, theft, or "mysterious disappearance," many will regret not purchasing specialized jewelry insurance.

If you have jewelry insurance, make sure you can replace your most prized possessions without having to pay a substantial amount of money out of pocket.

With all the choices you have for specialized jewelry insurance, don't wait. It only takes a minute to get a customer quote from a company like BriteCo. See for yourself how fast and easy you can get great coverage in this digital age.

International Gem Society

Related Articles

Marketing Your Gems Online

Advice for Determining Gemstone Value

Negotiating Strategies for the Gem Trade

Product Review, Opal Smart Chart

Latest Articles

Classic Engagement Ring Stones

Broken Bangle — The Blunder-Besmirched History of Jade Nomenclature: Book Review

Cuprite Value, Price, and Jewelry Information

Gemstone Radiation Treatment

Never Stop Learning

When you join the IGS community, you get trusted diamond & gemstone information when you need it.

Get Gemology Insights

Get started with the International Gem Society’s free guide to gemstone identification. Join our weekly newsletter & get a free copy of the Gem ID Checklist!